Chapter 10 — Central banks: the silent giants

In April 2022, two months after Russian forces crossed into Ukraine and six weeks after the G7 froze roughly $300 billion of Russian central bank reserves held in Western jurisdictions, the gold market changed.

Not on any given day. Not in any single headline. But across the central banks of every non-G7 country that watched what happened to Russia, a quiet recalculation began. If dollar reserves can be confiscated by political decision, then dollar reserves are not safe. Across the next 18 months, central banks bought gold at the fastest sustained pace since the early 1970s. China, Turkey, India, Poland, Singapore, the Gulf states, several African central banks, several South American ones — together absorbing roughly 1,000 tonnes a year of new physical gold demand. The Western retail flow signal that had dominated price discovery for two decades got drowned out.

This chapter is about that buyer. Who they are, how they buy, what they want, what stops them, and why their behavior is the single most important driver of the current gold regime.

Who holds the gold

Central banks collectively hold roughly 36,000 tonnes of monetary gold reserves at time of writing — about 17% of all gold ever mined. The distribution is concentrated. The top 10 holders, in order, are:

| Rank | Country / institution | Approx. tonnes |

|---|---|---|

| 1 | United States | 8,133 |

| 2 | Germany | 3,355 |

| 3 | Italy | 2,452 |

| 4 | France | 2,437 |

| 5 | Russia | 2,330 |

| 6 | China (reported) | 2,280 |

| 7 | Switzerland | 1,040 |

| 8 | Japan | 846 |

| 9 | India | 854 |

| 10 | Netherlands | 612 |

The top six hold the vast majority of the global central bank gold stock. But the change in holdings is what matters for the market, and the change is concentrated almost entirely in the EM central banks lower in the list.

The Western reserve holders — the US, Germany, Italy, France, Switzerland, Netherlands, Japan — have not materially changed their gold holdings in over 20 years. They hold legacy reserves from the Bretton Woods era and earlier. They neither buy nor sell. They are, in market terms, inert.

The buyers, the ones moving the market, are: China (publicly, since 2022, plus a structurally suspected but unverified parallel buying program), Turkey, India, Poland, Singapore, the UAE, Saudi Arabia, Qatar, Kazakhstan, and a long tail of smaller central banks that collectively add up to meaningful tonnes. The pattern: governments that are politically non-aligned with the G7, that hold high dollar reserve exposure, and that have explicit or implicit policy mandates to diversify away from that exposure.

How a central bank buys

A central bank does not call a retail broker. The mechanics:

- The LBMA market. Most central bank purchases go through the bullion banks (Chapter 8). The central bank's reserve management arm calls a market-making bank, requests a quote on a specific tonnage, and either accepts or rejects. The bank fills the order through its own inventory or by buying in the OTC spot market. Trades typically settle in 2 business days into the central bank's allocated London vault account.

- Domestic production. Several central banks (notably China and Russia, but also some smaller producers) buy directly from their domestic mining industry. The state pays the miner in local currency at the LBMA reference price; the gold flows into the central bank's domestic vaults. This route doesn't show up in LBMA flows.

- Bilateral swaps. Occasionally a central bank will lease gold to another central bank or to the BIS, swap gold against another reserve asset, or unwind such a swap. These transactions are reported with significant lags, sometimes only in BIS quarterly reviews.

- The BIS itself. The Bank for International Settlements (in Basel) operates as a banker to central banks and intermediates significant gold transactions on their behalf. The BIS publishes aggregate gold positions but does not disclose counterparties.

The reporting cadence varies. The IMF's Special Data Dissemination Standard (SDDS) requires monthly disclosure of reserve composition by participating central banks. Most major buyers (China, India, Russia, Turkey, the Gulf states) participate. The data is published with a 1-3 month lag. The People's Bank of China, specifically, updates its reserves in the first week of each month for the previous month-end position — this is the single most-watched central bank data point in the gold market.

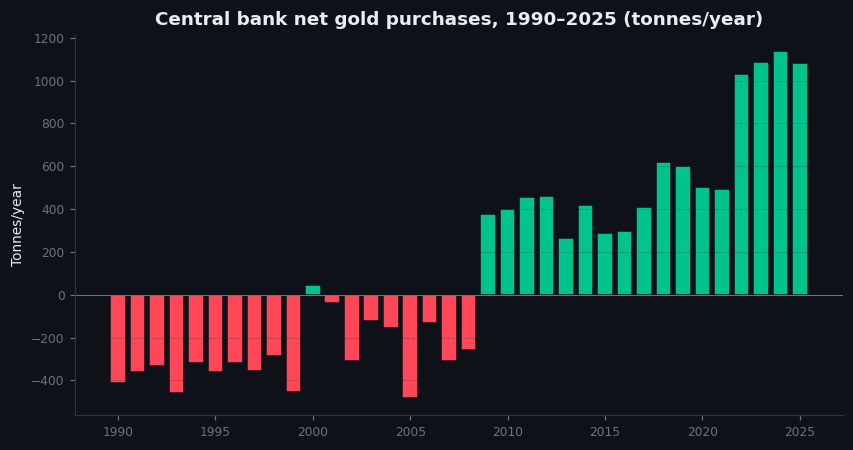

Figure 10.1 — Central bank net gold purchases, 1990–2025

Bar chart. Annual aggregate net gold purchases by all central banks, 1990 to 2025. Bars red for net selling (predominantly 1990s through 2008), green for net buying (2009 onward). Visible: regime change in 2009 from structural selling (driven by European reserve sales) to structural buying. Acceleration from 2018-2019 onward. The 2022-2025 step-change in pace (~1,000 tonnes annually, three times the 2010-2021 average) clearly marked. Side annotations naming the largest buyers in each year.

Illustrative — illustrative — annual CB flows calibrated to WGC history.

Why they buy

The motivations are not what most Western analysts think they are.

The mainstream Western framing — that central banks buy gold as an inflation hedge — is mostly wrong. Central banks do not hold gold to hedge against inflation. They hold gold for three reasons, in roughly this order of importance:

-

Counterparty independence. Dollar reserves require trust that the issuer will honor them. Treasury bills can be frozen. Bank deposits can be sanctioned. Gold sitting in a domestic vault, or in the BIS in Basel, has no counterparty. It is the only major reserve asset that does not depend on the political goodwill of a foreign government.

-

Portfolio diversification. Most central bank reserve portfolios are dominated by dollars, euros, and short-duration bonds. Gold has historically had low correlation with these, so adding gold lowers portfolio volatility for any given expected return. The standard portfolio theory case for gold as a reserve asset.

-

Long-term store of value. Over very long time horizons (multi-decade), gold has held its purchasing power against fiat currencies. Most central banks do not need this property in the short run, but it is the deep justification for treating gold as monetary, not commodity.

The 2022 Russia sanctions catalyzed a rapid increase in the weight of motive #1 in central bank reasoning. The argument that gold reserves are "barbarous relics" — the famous Keynes phrase — became indefensible the moment $300 billion of someone else's reserves were unilaterally frozen. Every central bank in the world re-ran its risk model. The ones that were already buying accelerated. The ones that weren't started.

What it takes to stop the buying

The current pace of central bank buying (~1,000 tonnes annually) is sustainable for a long time but not indefinitely. Three things could materially slow it:

- Reaching target allocations. Most EM central banks target gold at 10-25% of total reserves. Many are still below 10%. Once they reach their targets, the structural flow slows from "build" to "maintain." Estimates of when the largest buyers reach their targets vary, but most point to 2027-2030 for the dominant buyers, with a long tail of smaller central banks still building beyond that.

- A geopolitical de-escalation. If the political environment that made dollar reserves feel unsafe reverses materially — a US administration that explicitly walks back the willingness to use reserve sanctions, a stable G20 framework on reserve confiscation, something genuinely structural — the urgency of the diversification trade fades. This is, at present, not happening.

- A dramatic price spike. Central banks are price-insensitive within a wide range, but they are not infinitely so. A gold price that doubled in 18 months without any change in macro fundamentals would likely cause some buyers to pause and reassess. The 2024-2026 rally has tested this threshold; so far the buyers have continued.

A trader who wants to know when the current regime might be ending should watch for one of these three signals. None has appeared so far.

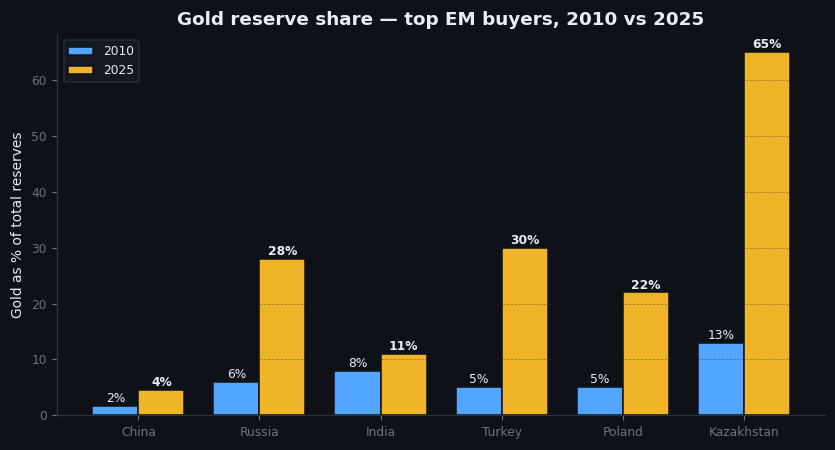

Figure 10.2 — Gold as percentage of total reserves, top EM buyers, 2010 vs 2025

Grouped bar chart. Countries on the x-axis (China, Russia, Turkey, India, Poland, Singapore, Saudi Arabia, UAE). Two bars per country: gold as % of total reserves in 2010, and the same in 2025. Visible: every country has materially increased its gold weight; most are still below the 25% level that several have stated as a target. The arithmetic implication for the remaining buying program is the right-hand side of the chart.

Illustrative — illustrative reserve-share comparison, calibrated to IMF / national CB filings.

On goldintel today

The dashboard does not yet have a dedicated central bank panel. This is a gap that, given the current regime's structure, should be closed. The nearest substitute is the news feed, which surfaces PBoC monthly reserve updates and major World Gold Council central bank data releases when they hit. Look for headlines tagged "central bank," "PBoC," "reserves," or specific country names in the buying cohort.

When PBoC reserve data shows a non-zero monthly buy, the price typically responds within 5-10 trading days. The dashboard's news scoring should pick these up; if you see one, treat it as a meaningful directional signal — not a reason to chase the immediate spike, but a reason to favor longs over shorts for the following week.

Common mistakes

- "All central banks buy gold." They do not. The G7 central banks are inert holders. The buying is concentrated in EM central banks with specific political and reserve-allocation motivations.

- "Central banks buy as an inflation hedge." They buy primarily for counterparty independence and portfolio diversification. Inflation hedging is a distant third reason.

- "Central banks will sell if prices keep rising." Historically they have not. Central banks are price-insensitive within wide ranges and trade on multi-year mandates, not on price levels.

- "PBoC data is unreliable." It is officially reported but widely suspected to understate true buying (gold from domestic Chinese miners may go to state-owned non-PBoC entities that are functionally state reserves but reported separately). The reported figure is a lower bound, not a complete picture.

Key takeaway

Central banks are the structural buyer that defines Regime 6. They are price-insensitive, mandate-driven, and unlikely to stop until they reach target allocations. Until then, they are the floor under the gold market.

Further reading:

- World Gold Council, Central Bank Gold Reserves annual report.

- IMF, Special Data Dissemination Standard — reserve composition disclosures by participating countries.

- Bank for International Settlements, Quarterly Review, central bank reserve sections.

- For PBoC specifically: Koos Jansen / BullionStar research on the discrepancy between official PBoC reports and total Chinese state gold accumulation. Contested but worth reading.