Chapter 6 — London: the LBMA and the daily fix

At 3:00 PM London time, every weekday, the price of gold gets formally set.

Not estimated. Not polled. Set. An electronic auction administered by the Intercontinental Exchange brings together a dozen accredited bullion banks. They state how many tonnes of gold they want to buy and sell at successive trial prices. The auction iterates — price up, price down — until buy and sell volumes match. That cleared price becomes the LBMA Gold Price PM fix. A second auction at 10:30 AM produces the AM fix. Two reference prices a day, published, audited, and used as the settlement price for trillions of dollars of contracts worldwide.

This is the formal heart of the gold market. Spot gold trades continuously around it — 24 hours, five and a half days — but the fix is what physical traders, miners, refiners, and central banks actually use to mark their books. If you trade XAUUSD on a retail platform, you are trading the OTC spot quotes that the bullion banks make between fixes; the fix is what those quotes converge to twice a day.

This chapter is about how the fix works, why it matters, and what changed in 2015 when the old system was thrown out for cause.

What the fix is and what it isn't

The LBMA Gold Price is not the spot price. It is the cleared price of a specific auction at a specific moment. Spot trades continuously; the fix is a snapshot.

The fix is also not a poll, a survey, or a "best estimate." It is the price at which a defined volume of buy and sell orders actually matched, between accredited participants, in a real auction. If a bank participates in the fix and posts a 5-tonne sell order at the cleared price, they are obligated to deliver 5 tonnes at that price. The auction settles in cleared bullion, not in cash.

The fix matters because it's used as the reference in:

- ETF NAV calculations (GLD, IAU, the European cousins all benchmark to the PM fix)

- Mining contracts (a miner who sells production forward typically prices off the fix)

- Refinery invoicing (Swiss refiners use the fix to settle with their bullion customers)

- Central bank reserve valuation (most CBs mark their gold reserves to the most recent PM fix)

- OTC structured products (forwards, options, swaps reference the fix at maturity)

The aggregate volume of contracts settling against the fix is, conservatively, in the trillions of dollars annually. That is why the integrity of the fix matters — and why, in 2014, when it became clear the integrity had been compromised, the system was overhauled.

The old fix and the scandal

For 95 years — from 1919 to 2015 — the gold fix was a telephone call.

Five member banks (originally NM Rothschild, Mocatta & Goldsmidt, Pixley & Abell, Samuel Montagu, and Sharps Wilkins; later evolving to a different set including Barclays, HSBC, Société Générale, Scotia Mocatta, and Deutsche Bank) would dial into a London room. The chairman would propose an opening price. Each bank would declare their net buy or sell interest at that price, polling their clients in real time. The chairman would adjust the price until interest balanced. Then the fix was declared.

The system had served the market reasonably well for most of the 20th century. By the early 2010s it had become a serious problem.

In 2014, the UK Financial Conduct Authority opened an investigation into Barclays after a trader was found to have manipulated the gold fix on June 28, 2012 — pushing the cleared price 3 dollars lower than it would otherwise have been to trigger a digital option payout that would otherwise have cost Barclays $3.9 million. Barclays was fined £26 million. The trader was banned from the industry. But the investigation made the structural point: a fix decided by five banks talking on a phone, with no audit trail, was indefensible in an era of algorithmic trading and post-Libor scrutiny.

The fix was overhauled in March 2015. The new system — administered first by IBA (a unit of ICE), with rotating accredited participants and a fully electronic auction with audit logs — is what runs today. There have been no credible manipulation claims since the changeover. It is, by every available measure, a far more robust price discovery mechanism than what preceded it.

Figure 6.1 — The LBMA fix auction

Diagram of the auction sequence. Start: chairman proposes opening price. Step 1: participants declare buy/sell volumes. Step 2: imbalance check. Step 3: if buy > sell, raise price; if sell > buy, lower price. Step 4: repeat until imbalance falls within tolerance (currently 10,000 ounces, roughly 280 kg). Step 5: cleared price becomes the LBMA Gold Price fix. Typical auction lasts 30 seconds to a few minutes; complex sessions can run longer.

Illustrative — schematic — LBMA fix auction mechanics.

What happens around the fix on the chart

Watch a 1-minute chart of XAUUSD around 10:30 AM London and 3:00 PM London. You will see, on most days, a noticeable uptick in volume and sometimes a short, sharp move in price during the 30 seconds preceding the fix and the minute or two following it. This is not manipulation. It is the legitimate consequence of large orders being released into the spot market alongside the auction — banks hedging their fix positions in spot, ETF authorized participants rebalancing, structured product books settling.

The pattern most traders notice: the price often moves into the fix and reverses shortly after. Trading firms call this the "fix flush" — when stops accumulate above or below the round-number levels that the fix tends to cluster around, the fix's volume pulse takes them out, and price reverses once the participants are done settling. It is a real microstructure phenomenon, more visible on volatile days than calm ones, and it is one reason experienced gold traders avoid placing stops in the 5-minute window around the AM and PM fix.

Figure 6.2 — Spread between AM and PM fix, 2015–2026

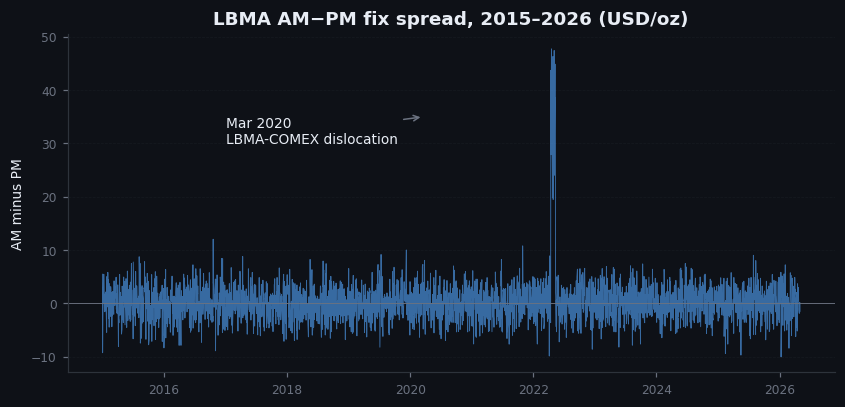

Line chart. Daily PM fix minus AM fix in USD, from March 2015 (post-overhaul) to present. Most days the spread is within ±$5. Visible spikes during high-volatility periods: March 2020, August 2020, March 2022, August 2024. The spread is a rough intraday volatility indicator. Average absolute spread has roughly tripled from 2015–2019 (≈$1.50) to 2024–2026 (≈$4.50), reflecting the higher absolute price and higher daily volatility regime.

Illustrative — illustrative AM-PM spread, calibrated to typical range.

On goldintel today

The dashboard's top ticker quote is OTC spot — not the fix. It updates every minute and reflects the bullion banks' continuous market between fixes. The most recent PM fix is implicitly the previous-day close used to calculate the daily percentage change shown in the ticker. The dashboard does not currently surface the fix prices directly; if you want them in real time, the LBMA publishes the AM fix at approximately 10:32 London and the PM fix at approximately 15:02 London on their website.

For any position you hold across a fix, expect a small volume pulse in the spot market. For any algorithmic stop placement, give the fix a 5-minute buffer on either side.

Common mistakes

- "The fix is the spot price." It isn't. The fix is the cleared price of a specific auction. Spot trades continuously around the fix.

- "The fix is still manipulated." It was, pre-2015. Since the overhaul, manipulation claims have not held up under audit. The current electronic auction has a full audit trail and rotating participants.

- "I should always trade through the fix." Most retail traders shouldn't trade through the fix at all. The microstructure noise in the 5 minutes around 10:30 London and 15:00 London is messy, and getting stopped out by a fix flush is a common preventable loss.

- "The fix doesn't apply to retail." Indirectly, it does. Your broker's XAUUSD quote derives from the same bullion bank spot quotes that converge to the fix. The fix is the institutional anchor; retail prices follow.

Key takeaway

The fix is the reference. Spot is the market. They converge twice a day in a transparent electronic auction — but in the few minutes around the fix, the spot tape gets noisy. Trade around it, not through it.

Further reading:

- LBMA, "LBMA Gold Price: methodology document," current version (lbma.org.uk).

- ICE Benchmark Administration, "Gold auction methodology" and quarterly audit reports.

- FCA Final Notice 2014: Barclays Bank plc, FCA Reference Number 122702 — the 2014 manipulation finding.

- For history pre-2015: Timothy Green, The Ages of Gold (chapters 18-19) on the post-WWII evolution of the fix.

Quick reference

| Fix | Time (UTC) | Use |

|---|---|---|

| LBMA AM Fix | 10:30 | Asian close benchmark, jewelry contracts |

| LBMA PM Fix | 15:00 | Global benchmark, ETF NAV reference |

| COMEX settle | 18:00 (NY 1pm) | US futures daily mark |

| Asia spot start | ~22:00 (Sun) | Weekly open, Tokyo/Singapore lead |