Chapter 7 — New York: COMEX, futures, and basis

If London is where gold gets settled, New York is where gold gets priced.

The COMEX gold futures contract — symbol GC, 100 troy ounces, traded on the CME Globex platform — is the single most-traded gold instrument in the world. On a typical day, a quarter of a million GC contracts change hands. That is 25 million ounces, or roughly 770 tonnes — more than ten times the daily volume of physical gold movement through London. The GC price is what every algorithm watches. The London fix gives you the institutional reference; COMEX gives you the price.

For a trader who only watches XAUUSD spot, this matters because COMEX is upstream of spot. When spot moves, it usually moves because GC moved first. When you see a sharp 60-second move on your XAUUSD chart at 8:30 AM New York time, it is almost certainly a COMEX algo response to a data release that the spot quote is catching up to.

This chapter is about how COMEX works, how it relates to spot, and the two concepts — basis and open interest — that every gold trader should understand before placing a serious trade.

What a futures contract is, mechanically

A COMEX gold futures contract is an obligation to deliver (or receive) 100 troy ounces of Good Delivery gold on a specific future date at a specific price. The standard contract months are even-numbered (Feb, Apr, Jun, Aug, Oct, Dec), plus a few odd-numbered months for shorter-dated needs. The most-traded contract at any moment is the "front month" — typically the second nearest even-numbered month, because the very nearest one is in active delivery.

You can trade a futures contract two ways:

- Speculatively. You enter long or short, hold for some period, and exit by buying back or selling out before delivery. The vast majority of contracts (well over 99%) are closed this way. You never see physical gold. Your account is debited or credited the price difference.

- For delivery. You hold the contract through its delivery date and either take delivery (long) or make delivery (short). This is what miners, refiners, central banks, and some institutional investors do. The contract specifies how delivery happens — registered warehouse receipts at approved COMEX vaults in New York, plus a small set of secondary depositories.

The two ways are linked. Even though speculators dominate, the fact that the contract can be delivered keeps the futures price anchored to the physical price. A futures price that drifts too far from spot creates a free-money arbitrage — buy spot, sell future, deliver into the future, pocket the difference. That arbitrage is what holds the basis tight.

Basis, contango, and backwardation

The basis is the difference between the futures price and the spot price.

In a normal gold market the basis is positive — futures trade higher than spot. This is called contango. The math is straightforward: holding physical gold costs money (storage, insurance, financing). To make a forward delivery worthwhile to the seller, the futures price must compensate for those costs. In equilibrium:

Futures price ≈ Spot price + (cost of carry × time to delivery)

The cost of carry on gold is roughly the dollar interest rate minus the gold lease rate. When dollar rates are 5% and gold lease rates are zero, the cost of carry is about 5% annualized — so a contract three months out should trade roughly 1.25% above spot.

When the basis goes negative — futures trading below spot — the market is in backwardation. This is unusual for gold (much more common in crude oil and agricultural commodities, where supply can be physically constrained). For gold, backwardation usually signals one of two things:

- Physical tightness. Vault inventories are low; market participants are willing to pay a premium for immediate delivery over future delivery. This was visible during the 2020 LBMA-COMEX divergence and during several periods in 2008-2009.

- Lease rate spike. When gold lease rates rise sharply (a different bullish signal we will cover in Chapter 8), the cost of carry collapses and the futures-to-spot relationship inverts.

Backwardation in gold is rare and almost always bullish. A trader who watches the basis can spot stress in the physical market before it shows up in the price.

Open interest

The other COMEX number worth watching is open interest — the total number of futures contracts outstanding at the end of each trading day. It is published daily by the CME, broken down by contract month.

Open interest at the time of writing is roughly 450,000 GC contracts, equivalent to 1,400 tonnes of gold notional. The interpretation:

- Rising open interest plus rising price = new money is going long. Healthy uptrend.

- Rising open interest plus falling price = new money is going short. Healthy downtrend.

- Falling open interest plus rising price = shorts are covering. Often a late-stage rally, watch for exhaustion.

- Falling open interest plus falling price = longs are liquidating. Often a late-stage decline, watch for capitulation.

This is not a precise signal but a directional one. Combined with the COT report (Chapter 26), open interest gives you a read on whether the move you are seeing has fresh money behind it or is being driven by position-unwinding.

Figure 7.1 — COMEX gold open interest vs price, 2015–2026

Two-panel chart. Top panel: monthly gold price. Bottom panel: total COMEX gold open interest in contracts. Annotations showing the four pattern combinations (rising OI + rising price, etc.) at specific historical moments. Particular attention to the 2020 collapse in OI during the LBMA-COMEX divergence (open interest fell from 800k to 480k contracts as the EFP mechanism broke).

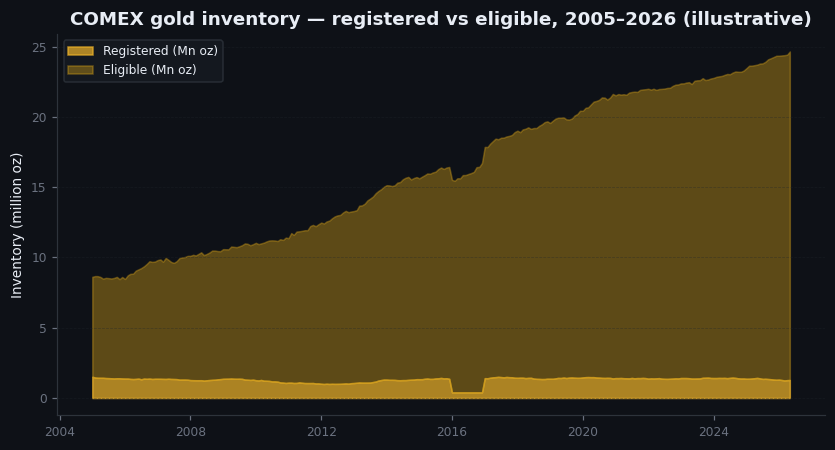

Registered vs eligible gold

A peculiarity of the COMEX gold inventory worth knowing: the vaults distinguish between registered and eligible gold.

- Eligible gold is in the COMEX-approved vaults in the proper bar size (mostly 100-ounce bars; kilobars are also accepted under specific rules), but is not warranted for delivery against an open futures contract. It is privately owned, parked at a COMEX vault for storage.

- Registered gold has an active warehouse receipt — a warrant — that makes it deliverable against a futures contract. A long who holds through delivery receives a warrant on registered gold.

At time of writing, COMEX has roughly 600 tonnes of total gold inventory across all vaults, of which approximately 100 tonnes is registered. Open interest is roughly 1,400 tonnes notional. The math seems alarming: 1,400 tonnes of contracts versus 100 tonnes of immediately-deliverable gold.

It works because almost no one takes delivery. Speculators roll. Eligible gold can be re-registered if delivery demand spikes — owners simply file the paperwork to convert it. And in extremis, EFP (the swap mechanism described in Chapter 1) converts a COMEX contract into a London-vaulted bar. The system has held for 50 years. But the registered-versus-eligible ratio is something to watch during stress — when registered inventory falls below 5% of open interest for sustained periods, the market is telling you something.

Figure 7.2 — COMEX registered and eligible gold inventory, 2005–2026

Stacked area chart. Two layers: eligible gold (light) and registered gold (dark). Visible structural decline in registered gold as a percentage of total from 2013 onward. Annotations at the 2016 and 2020 troughs where registered inventory fell to historically low levels.

Illustrative — illustrative — COMEX registered/eligible inventory trend (CME paid data).

On goldintel today

The dashboard does not currently surface COMEX data directly — no basis, no open interest, no inventory. This is a gap that, given how important the data is, should be closed. For now, the cleanest source is the CME's daily Gold Futures Summary email (free, requires CME account) and the COT report (Chapter 26) which we do partially reflect through the news feed when major positioning changes are reported.

If you trade XAUUSD off the dashboard, keep a TradingView tab open on GC1! (the continuous front-month contract) for cross-reference. When XAUUSD and GC1 diverge by more than a few cents, that is information worth investigating.

Common mistakes

- "Spot is the real price." Spot follows COMEX in the short term. The price discovery happens in GC; spot is downstream.

- "I don't need to think about basis." If you trade with a holding period longer than a few days, you should. Roll costs in contango eat into a long position's return. In strong contango, holding a gold long via futures (or a gold-futures-tracking ETF) costs ~5% annualized.

- "COMEX could be cornered." Theoretically possible. Practically prevented by margin rules, position limits, and the EFP escape hatch. The 1980 Hunt silver corner is the relevant case study; the rules have tightened significantly since then specifically to prevent recurrence.

- "Open interest is just noise." It isn't. Direction of open interest, combined with direction of price, tells you whether the move is fresh money or position unwinding. That's important.

Key takeaway

COMEX is where the gold price is made; spot is where it is settled. Watch the front-month futures, the basis, and open interest as a single complex. They tell you what kind of move you're in before the chart does.

Further reading:

- CME Group, "Gold Futures: Contract Specifications and Trader's Guide," current edition.

- Hilary Till and Joseph Eagleeye (eds.), Intelligent Commodity Investing. Chapter on basis and roll yields applies cleanly to gold.

- For the historical context on registered/eligible inventory: Ronan Manly's running analyses at BullionStar — long-form, occasionally polemical, but accurate on the mechanics.

- CFTC's weekly Commitment of Traders report, gold section.

Quick reference

| Contract | Size | Tick | Tick value | Use |

|---|---|---|---|---|

| Gold (GC) | 100 oz | $0.10 | $10 | Standard institutional |

| Mini Gold (QO) | 50 oz | $0.25 | $12.50 | Smaller funds |

| Micro Gold (MGC) | 10 oz | $0.10 | $1 | Retail, scaling-in |

| E-mini (YG) | 33.2 oz | $0.10 | $3.32 | ICE alternative |